Registration is open for NSPECon26 in New York City, New York!

Registration is open for NSPECon26 in New York City, New York! Volunteering at NSPE is a great opportunity to grow your professional network and connect with other leaders in the field.

Volunteering at NSPE is a great opportunity to grow your professional network and connect with other leaders in the field. Decisions at the ballot box influence policies that support engineering standards and public safety.

Decisions at the ballot box influence policies that support engineering standards and public safety.

Each year the National Society of Professional Engineers (NSPE), American Institute of Architects (AIA), and the American Council of Engineering Companies (ACEC), conduct a consolidated risk management survey of professional liability insurance carriers (Carriers). The survey compiles information about trends in coverage, coverage options, exclusions, claims, and risk management practice across the industry. The survey also allows NSPE, AIA, and ACEC to evaluate each Carrier’s history in providing insights into trends affecting professional liability insurance. The full survey can be accessed in the Professional Resources section of the NSPE website.

In 2025, nearly all participating Carriers describe the architecture and engineering (A&E) professional liability insurance market as stable, competitive, and buyer-friendly. Yet Carriers caution that several underlying pressures like rising claim severity, climate-driven expectations, workforce challenges, technology adoption, and evolving project delivery models are beginning to reshape exposure in ways that firms (and individuals tasked with risk management within those firms) must anticipate.

Complex Claims

While claim frequency remains relatively stable, claim severity continues its multi-year climb. Carriers cite social inflation, litigation funding, and increasingly plaintiff-friendly jurisdictions as primary drivers. Carriers report that claim severity has increased, particularly in matters involving multiple parties or disputes tied to large infrastructure, transportation, or mixed-use residential projects. These claims take longer to resolve, involve more parties, demand greater resources, and often result in larger settlements.

These cases often take longer to resolve than they did several years ago, with some Carriers noting that what once might have been an 18-month process can now take three to five years. Factors such as construction delays, cost escalation, and continued pandemic-related impacts influence the timelines and costs associated with resolving disputes. Bodily injury claims, structural engineering errors, and multi-use residential construction issues also continue to generate high-severity losses. Luxury residential and mixed-use condominium projects stand out as a growing exposure, with escalating costs and high-value claimants combining to magnify the financial stakes.

Carriers also point out that staffing transitions within firms can contribute to errors that later lead to claims. As firms face tightened labor markets, younger and less experienced professionals may step into demanding roles more quickly. Errors arising from insufficient oversight have become a common trigger for losses reaching policy limits.

Market Stability Masks Emerging Pressures

Despite these challenges, professional liability insurance pricing has not tightened significantly. Carriers attribute this to abundant capital, a competitive marketplace, and a stable overall frequency of claims. But several caution that this balance is delicate. A sustained increase in high-severity losses, particularly involving bodily injury, could change the picture quickly.

Project-specific insurance is another pressure point. Some Carriers note rising claims emerging from these arrangements, especially in aggressive design-build environments or on projects with substantial private equity or concessionaire involvement. While project-specific professional liability insurance is available, the market shows a preference for keeping risks within practice policies unless project demands, or owner requirements, necessitate higher limits.

Carriers report that higher limits are an increasingly frequent request. With construction inflation raising the value of projects, owners often seek $5 million to $10 million or more in coverage. Excess layers are becoming more common as well. When owners seek higher insurance limits from prime consultants, the prime consultants often must seek higher limits from subconsultants.

Climate and Environmental Impact

Carriers consistently mentioned the growing impact of climate-related risk. Climate-related risks are forcing design professionals to adapt practice beyond typical code requirements. Carriers emphasized that code is increasingly a floor, not a ceiling, and that professionals must be cautious in their practice when only meeting code minimums and not necessarily analyzing climate-related risk of a project design decision. For now, Carriers encourage firms to document project assumptions and conversations (internal and with the client) clearly when climate resilience and code requirements are part of the discussion.

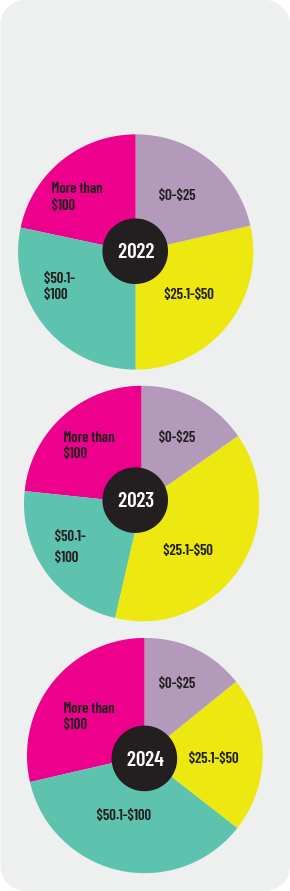

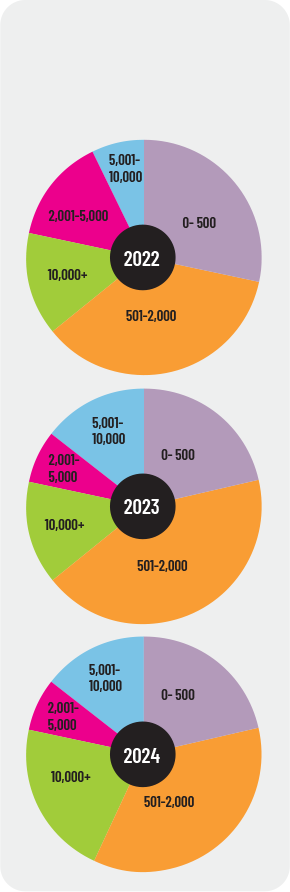

What was your total premium from engineering and architectural liability insurance in the following years? (in millions)

Perfluoroalkyl and polyfluoroalkyl substances (PFAS), for example, has emerged as a topic many Carriers are monitoring, particularly with regulatory reporting requirements expected in the coming years. Some environmental liability policies have begun to include PFAS-related exclusions, and Carriers anticipate that questions about PFAS may become more common. However, Carriers also note that PFAS-related professional claims remain relatively limited, and they are still evaluating how much of an impact this issue may ultimately have on design professionals.

Emerging Technologies

The growing use of artificial intelligence (AI) in engineering workflows is another area where Carriers are paying increased attention. Carriers consistently describe AI as a tool with which firms are experimenting, primarily in drafting, research, and preliminary analysis. Carriers report that most underwriters say they are not yet incorporating AI into underwriting criteria, but they are beginning to ask firms how they supervise and review AI-assisted work. Several Carriers noted that they expect questions about AI to expand over time, particularly around topics such as copyright, data sources, and quality control. The main message from Carriers is that licensed professionals remain responsible for verifying the accuracy of any work, regardless of whether AI played a role in producing it — just like they would when overseeing the work of an intern or draftsperson.

2025 Directory of Professional Liability Insurance Providers

AIG/LEXINGTON

Adam Reeser

1225 E. 17th Street, Suite 3150 Denver, CO 80202

267-666-8478

ALLIANZ

Glen Mangold 225 W. Washington

St, Suite 1800 Chicago, IL 60606

312-371-5933

ALLIED WORLD

Joshua Kranz

199 Water Street New York, NY 10038

917-587-7655

ASPEN INSURANCE

Robert Cunningham

499 Washington Blvd Jersey City, NJ 07310

917-213-6265

AXA XL

Michaela Kendall

3340 Peachtree Road NE, Suite 2140 Atlanta, GA 30326

404-439-6072

AXIS INSURANCE

Victoria Szot

P.O. Box 3384 Alpharetta, GA 30023

BEAZLEY

James K. Schwartz, Esq.

I Lincoln Street Boston, MA 02111

617-671-8016

BERKLEY DESIGN PROFESSIONAL

Thomas Rea

180 Glastonbury Blvd. Glastonbury, CT 06033

860-716-3859

BERKSHIRE HATHAWAY SPECIALTY INSURANCE

Joe Schrancz

620 West. Germantown Pike Plymouth Meeting, PA 19462

917-830-2322

EVEREST NATIONAL INSURANCE COMPANY

Ed Stitz

100 Everest Way Warren, NJ 07059

646-477-3951

PROFESSIONAL UNDERWRITERS AGENCY (PUA)

Sandip Chandarana

2803 Butterfield Road Suite 260 Oak Brook, IL 60523

630-572-0600

RIVERTON INSURANCE AGENCY CORP.

Lenny Waldhauser

600 Main Street Suite 2 Riverton, NJ 08077

800-882-4410

RLI

Vince Costello

150 Monument Road Bala Cynwyd, PA 19004

610-664-6763

THE HARTFORD

Jasmin Tatum

One Hartford Plaza Hartford, CT 06155

443-364-5951

TRAVELERS

John Rapp

10 North Park Drive Hunt Valley, MD 21030

443-353-2262

VICTOR INSURANCE MANAGERS, LLC

Kevin Collins

7700 Wisconsin Avenue, Suite 400 Bethesda, Maryland 20814

301-951-5412

Workforce and Project Delivery

Staffing remains a persistent risk concern across the A&E sector. Firms face challenges attracting and retaining experienced professionals The loss of seasoned staff increases oversight risk, slows project review cycles, and creates exposure. Project delivery models add layers of complexity. Designbuild continues to expand, and while it offers speed and efficiency, it also blurs responsibility boundaries. Aggressive design-build arrangements, in particular, have reportedly produced accelerated losses in several carrier portfolios.

Project delivery also continues to influence professional liability exposure. Some Carriers mentioned that design-build projects and certain public-private partnership (P3) structures may increase the responsibilities placed on design professionals, especially when schedule pressures or contractual terms introduce additional expectations. Although P3 activity does not appear to be dominating claim trends, several insurers noted that these arrangements can produce complicated claim scenarios when responsibilities are shared between concessionaires, contractors, and designers.

What to Focus on in 2026

Carriers consistently recommend several strategies in this evolving environment:

- Strengthen contract review and negotiation: Unilateral indemnity clauses, heightened standards of care, and overly broad scopes remain problematic. Carriers encourage regular contract reviews with some Carriers providing contract review services for clients.

- Document climate discussions: Silence in this area creates exposure. Clear written communication with clients is essential regarding scope and code compliance.

- Develop AI usage policies: Firms should establish internal guidelines for AI use, supervision, approval, and documentation.

Continue training and mentoring: Workforce turnover increases exposure; targeted skill development and appropriate project oversight protects the firm. - Maintain strong risk management and quality management practices: Strong risk and quality management can prevent or reduce losses.Continue to educate staff on risk fundamentals, contract terms and contract negotiations, and existing and emerging risk concerns. Continue to reinforce quality practices.

- Reassess insurance limits regularly: With project values rising, be proactive in reviewing and maintaining adequate insurance coverage relative to potential loss scenarios.

Do you offer a premium credit for membership in a professional society and/or trade association (e.g., ACEC, the AIA Trust, or NSPE)?

Do you provide multi-year policies?

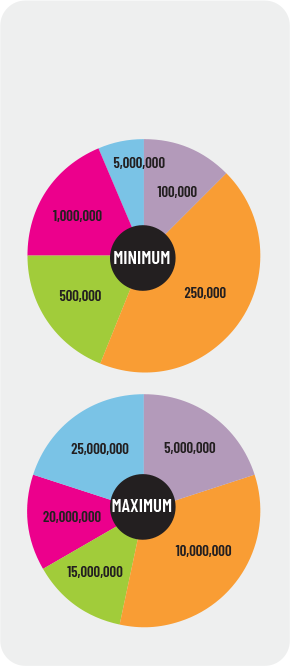

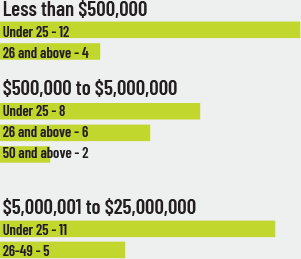

What limits of A/E professional liability coverage are available through your company?

Looking ahead, the 2026 professional liability environment presents a mix of stability and gradual change. The market remains favorable for most firms from a pricing and capacity standpoint, and Carriers continue to support engineering practices with a wide range of coverage options. At the same time, changes in claim behavior, climate expectations, technology use, and project delivery approaches suggest that firms should stay attentive to how these developments may influence their risk profiles and whether any of their current risk management strategies should be altered or augmented. While the environment is not marked by dramatic shifts, it is one in which thoughtful risk management and careful project documentation can help engineering firms navigate a steadily evolving landscape.

What was the total number of firms for which you provided engineering and/or architectural liability insurance in the following years?

Noelle Cochran, P.E. and F.NSPE, is a risk management director with AECOM where she supports multiple business lines in managing project risk. Cochran values sharing her risk management knowledge to help others improve project delivery and prevent loss.

Spencer Rojas is an attorney with Taft Stettinius & Hollister LLP. Rojas is based in the firm’s Minneapolis office.

Kodi J. Verhalen, ESQ., P.E., F.NSPE, is a partner in Taft’s Energy Practice Group, focusing her practice on a wide variety of electric and natural gas regulatory matters.

More Featured Articles

The United States leads the world in the number of quantum technology startups and global revenues are expected to reach $72 billion by 2035. The technology is still a mystery to the public, but can we solve the unsolvable with the "strangeness" of quantum computing?

It is important for professional engineers to understand and apply professional ethical standards in their work. While engineers do not struggle to distinguish right from wrong, they face obstacles when trying to influence leaders and their colleagues. A new study offers guidance on how to resist unethical requests and empower others to make the right decision. >>

Licensure exemptions make way for too many engineering projects that are conducted without the direction of PEs—whose paramount responsibility is public protection. The public, which thinks highly of engineers, is not aware that this subjects them to unnecessary risks. There are opportunities for the engineering community to unite to protect the public by reducing or eliminating licensure exemptions. >>

During the height of the COVID pandemic, the level of fear across the globe was unprecedented in living memory. Fortunately, there were a select number of engineers who could help during this time of crisis. Capt. Stephen Martin Jr., Ph.D., P.E., received the 2024 Federal Engineer of the Year Award for using his expertise during the pandemic. >>

The arrival of ChatGPT and other artificial intelligence systems has entered the public consciousness with a vengeance. This new tech is disorienting and raises many questions. How will these systems affect the world of work? Will they take over my job? How will they affect the practice of engineering? An analysis of the introduction of past technologies may offer guidance. >>

DiscoverE has released its latest research on the views of high school students and parents on engineering and engineering careers. The Messages Matter results were encouraging as they reveal that targeted messages and profiles of engineers can spur interest in engineering among the very groups that will ensure a more diverse future for the field. »

NSPE members and professional licensed engineers are stepping up to lead on creating sustainable and resilient communities. This issue of PE magazine offers insight on the role of the engineering community with climate change and puts a spotlight on a Vermont engineering college program that is nationally recognized for its zero energy design focus. »

It’s essential that professional engineers have access to all possible protections from frivolous lawsuits. NSPE pays close attention to proposed legislation, proposed regulations, and court cases affecting the profession. NSPE and state societies take action by reaching out to legislators and agencies to educate and explain the implications of language under consideration. »

NSPE’s Emerging Leaders Program supports the leadership growth of early-career professionals and helps them develop the skills needed to advance beyond the technical. The program’s graduates are taking their careers to the next level and pursuing opportunities to be engineering change makers. »